Something significant is happening in global finance right now — and it’s not about cryptocurrency speculation or NFTs. It’s about the plumbing of the world’s financial system getting a complete rebuild.

By 2026, three big technologies have gone from experimental side projects to mainstream infrastructure: tokenized real-world assets (RWAs), institutional-grade digital custody, and multi-central bank digital currency (mCBDC) payment platforms. Together, they’re replacing slow, expensive, and opaque legacy systems with something that works 24/7, settles in seconds, and costs a fraction of what it did before. Here’s a plain-language breakdown of what’s actually happening, why it matters, and what it means for the future of money.

Part 1: Turning Real Assets Into Digital Tokens

What Is Asset Tokenization?

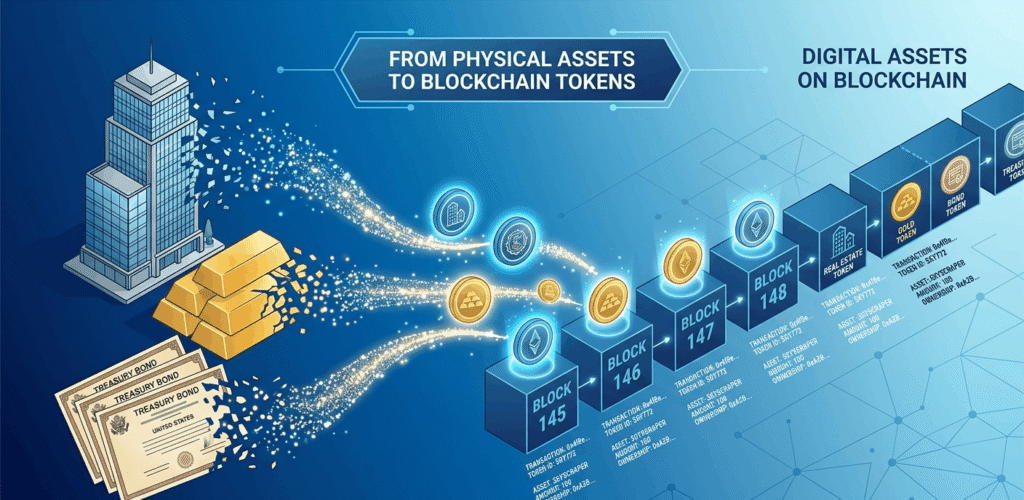

Think of tokenization as creating a digital copy of a real asset, a government bond, a piece of real estate, a gold bar, and putting it on a blockchain. Afterward, that digital copy can be traded, used as collateral, or even divided into smaller portions, allowing more people to own a share.

What used to take days to settle now takes minutes. What used to require millions of dollars to access can now be purchased for as little as $100.

How Big Is This Market?

By November 2025, the total value of tokenized real-world assets on-chain had reached approximately $35.9 billion. Analysts expect that number to exceed $100 billion by end of 2026, and potentially hit $30 trillion by 2034.

Some of the biggest categories right now include:

| Asset Type | Estimated Value | Why It’s Growing |

| Tokenized U.S. Treasuries | ~$9.6 Billion | Safe on-chain yield |

| Tokenized Gold | ~$7.0 Billion | Inflation hedge + 24/7 liquidity |

| Private Credit & Bonds | $1.5T market potential | Unlocking illiquid debt |

| Money Market Funds | ~$8.0 Billion | Real-time cash management |

The Real Benefits — Beyond the Buzzwords

Here’s what tokenization actually changes in practice:

Key Benefits

- Settlement speed: Bond trades that used to take 2 days now settle in under 10 minutes. Transaction fees dropped by more than 70% in major bank pilots.

- Fractional ownership: Investors can buy shares of commercial real estate or fine art for as little as $100, opening markets that were previously limited to the ultra-wealthy.

- Transparency: Every transaction is recorded on an immutable ledger. Platforms now offer ‘on-chain audits’ where asset performance — like rental income or bond payments — updates automatically and is visible to all authorized parties.

- 24/7 markets: Blockchain rails never close. Institutional investors can manage, trade, and settle around the clock, across time zones.

The Big Players Are Already In

This isn’t startup territory anymore.

- BlackRock’s BUIDL fund — a tokenized institutional money market product — surpassed $2 billion in assets under management by March 2026. BUIDL tokens are now being used as collateral in decentralized lending protocols like Morpho, bridging institutional money with on-chain finance.

- JPMorgan arranged a landmark commercial paper issuance on the Solana public blockchain for Galaxy Digital in December 2025, using USDC stablecoins for settlement — a significant push into public blockchain infrastructure.

- Goldman Sachs is reportedly planning to spin out its GS DAP tokenization platform into an independent, industry-owned company, signaling that blockchain infrastructure is becoming shared financial utility.

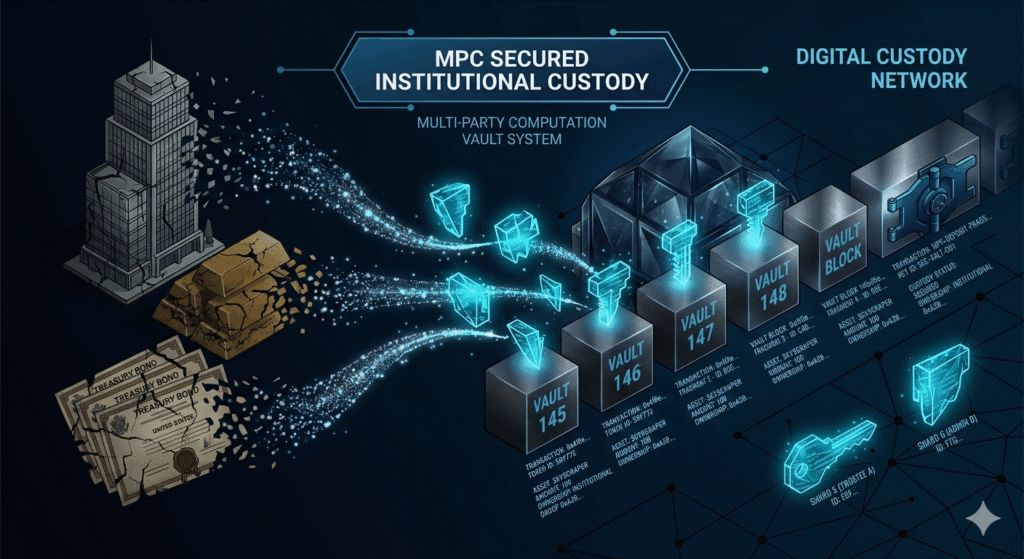

Part 2: Keeping Digital Assets Safe — The Custody Challenge

Owning a tokenized bond or digital asset is only half the story. The other half is keeping it safe — especially when we’re talking about pension funds, sovereign wealth funds, and the world’s biggest asset managers.

In 2026, crypto custody has matured from simple private key storage into a sophisticated suite of services that includes prime brokerage, staking, governance participation, and insurance.

Two Ways to Secure Digital Assets

Most institutional custodians use one (or both) of these approaches:

| Method | How It Works | Best For |

| Multi-Party Computation (MPC) | Splits the private key into encrypted shares held by multiple parties — no single point of failure. | Frequent transactions, market makers, exchanges. |

| Cold Storage (HSM) | Keys stored on offline hardware — completely disconnected from the internet. | Long-term holding, maximum security for pension funds and fiduciaries. |

Who’s Guarding the Assets?

The leading institutional custodians in 2026 include both crypto-native firms and traditional banking giants:

- Fidelity Digital Assets — Backed by $4 trillion in AUM. Received an OCC national trust bank charter in 2025. Rated lowest default risk in the industry at 0.39%.

- Anchorage Digital — The first crypto-native firm to receive an OCC federal bank charter. Can settle 90% of BTC/ETH transactions from cold storage in under 15 minutes.

- Coinbase Custody — Secures roughly 12% of total crypto market cap. Carries $320 million in insurance coverage against theft or loss.

- BitGo — Received its OCC bank charter in late 2025, filed for a $200 million NYSE IPO in early 2026, and crossed $90 billion in assets under custody.

- Zodia Custody — Backed by Standard Chartered and Northern Trust, focused on institutional governance and secured lending.

The Regulatory Shift That Made It All Possible

One key regulatory change unlocked the custody market: the SEC’s rescission of Staff Accounting Bulletin 121 (SAB 121). Previously, banks that held crypto on behalf of clients had to list those assets as liabilities on their own balance sheets — a huge disincentive. Removing that requirement allowed traditional custodians like BNY Mellon and State Street to scale their digital asset services significantly.

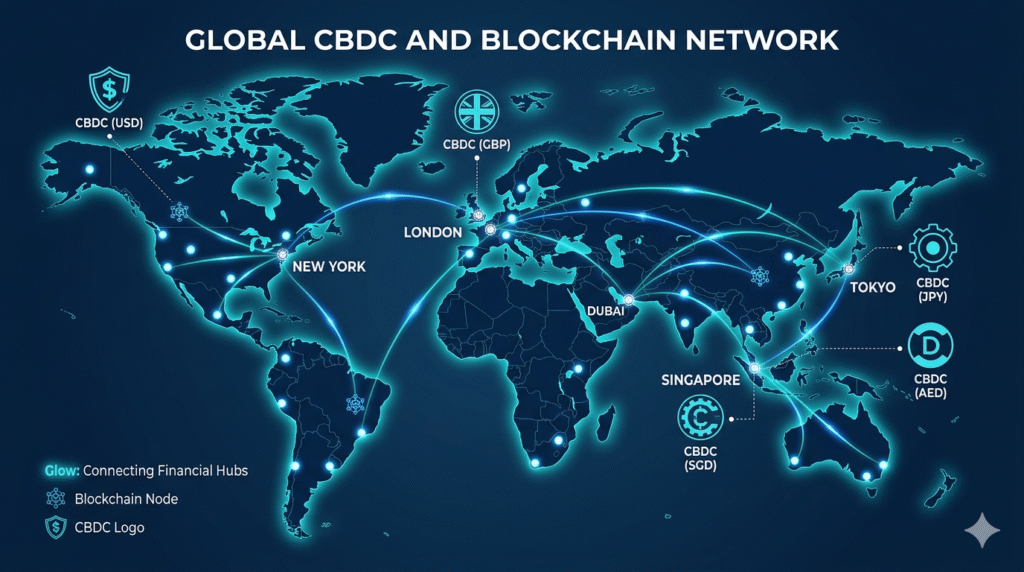

Part 3: Rethinking How Money Moves Between Countries

Cross-border payments are one of the most frustrating inefficiencies in global finance. Sending money internationally can take 3–5 days and passes through a chain of banks, each adding fees and compliance checks along the way. The market for cross-border payments moves between $140 trillion and $320 trillion annually — and the infrastructure handling it hasn’t fundamentally changed in decades.

Two major CBDC platforms are trying to fix this:

Project Agorá: The Western Approach

Project Agorá is a BIS-led initiative involving seven central banks — including the Federal Reserve Bank of New York, the Bank of England, and the Bank of Japan — along with 40+ private financial institutions. The goal: replace the clunky ‘relay race’ of correspondent banking with a single shared ledger where payments settle atomically (meaning money and assets swap at the exact same instant, with no risk that one side doesn’t deliver).

The project completed its testing phase in 2025 and is expected to publish final results in the first half of 2026. It focuses on wholesale interbank settlement — not something retail customers would use directly, but the infrastructure that underpins every international wire transfer.

Project mBridge: Already Live and Moving Billions

While Agorá is still finalizing, Project mBridge — involving China, Hong Kong, the UAE, Thailand, and Saudi Arabia — is already running at scale. By early 2026, it had processed more than 4,000 cross-border transactions with a cumulative value exceeding $55 billion.

China’s digital yuan (e-CNY) accounts for 95% of total settlement volume on mBridge. The platform is widely seen as a ‘de-dollarization’ infrastructure — a functional alternative to dollar-dominated payment systems. In late 2025, the UAE Ministry of Finance executed a government transaction using a wholesale digital dirham on the platform.

What About Stablecoins?

Stablecoins are becoming the internet’s dollar, with on-chain transfers hitting about $28 trillion in 2024. By 2025, $350–550 billion is expected to support real-world payments like cross-border business transactions and remittances.

The GENIUS Act sets clear rules for approved issuers, requiring full 1:1 asset backing and confirming stablecoins are not treated as securities.

Corporate treasurers are also adopting a strategy called the “stablecoin sandwich”:

| The Stablecoin Sandwich Step 1: Convert fiat currency into a stablecoin Step 2: Transfer the stablecoin instantly across borders via blockchain Step 3: Convert back into local fiat currency at the destination Result: Real-time settlement that bypasses correspondent banking entirely — and funds arrive ‘just in time’ for international subsidiaries. |

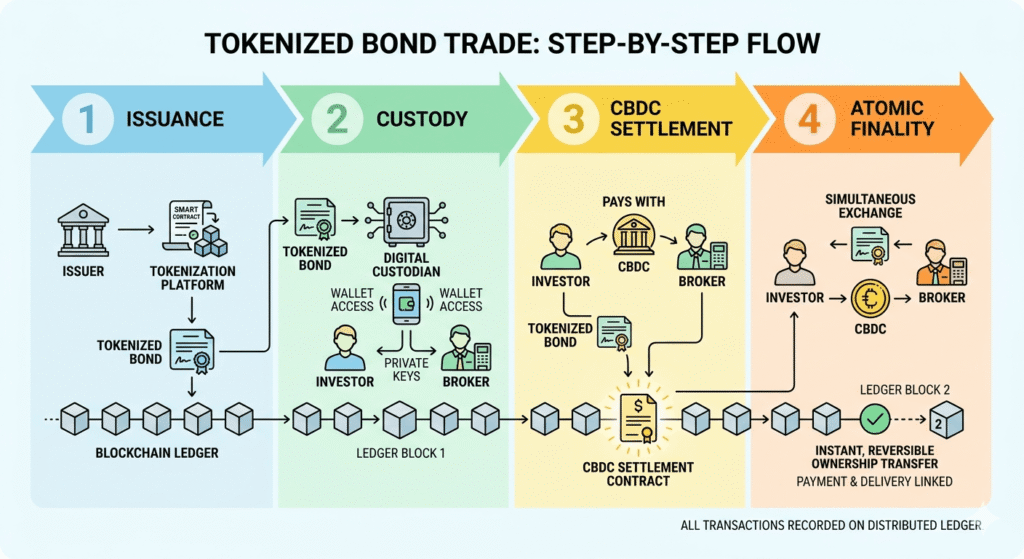

Part 4: How It All Connects — A Real Transaction in 2026

Here’s how all three pillars work together in a single trade:

Scenario: An institutional investor in Singapore buys a tokenized corporate bond from a European company.

| Step-by-Step Atomic Bond Settlement 1. Issuance: The bond is minted as a token on a programmable ledger (e.g., Ethereum or the Canton Network). KYC/AML rules and coupon payments are embedded directly in the smart contract. 2. Custody check: The investor’s qualified custodian (e.g., Anchorage Digital) uses an MPC system to verify the investor is authorized to hold the asset and that the trade complies with internal risk policies. 3. Multi-CBDC settlement: Payment is executed on a platform like Project Agorá. The investor’s tokenized Singapore Dollar deposit is exchanged for the bond; final settlement between banks happens in wholesale central bank money. 4. Atomic finality: The bond transfer and the payment happen at the exact same millisecond. If anything fails, the entire trade is voided — no risk that one party pays but doesn’t receive the asset. |

Part 5: The Rules Are Catching Up

One of the biggest reasons 2026 feels different is that regulators have finally given institutions the clarity they needed.

| Regulatory Development | What It Means in Practice |

| SAB 121 Rescission | Banks can now custody crypto for clients without inflating their own balance sheets. Traditional custodians can scale. |

| GENIUS Act (U.S.) | Payment stablecoins have a clear legal definition. They’re not securities, and issuers must back them 1:1 with liquid assets. |

| FASB ASU 2023-08 | Companies can now report digital assets at fair market value. This makes BTC and tokenized assets viable corporate treasury tools. |

| MiCA (EU) | A unified licensing framework for crypto custodians and issuers across all 27 EU member states. |

| SEC ‘Technological Neutrality’ | A tokenized stock is still a stock. The same registration rules apply — but so does the same capital treatment. |

What’s Still Being Figured Out

Despite the momentum, several challenges remain:

- Fragmented liquidity: Assets tokenized on Ethereum may not be easily usable on Solana or other chains. Cross-chain bridges exist but add security risk. Solving interoperability is the industry’s top priority right now.

- Cybersecurity: As more value moves on-chain, the stakes for a breach go up. Blockchain transactions are irreversible — there’s no ‘undo’ button. Institutions are responding with AI-powered fraud detection and multi-person approval workflows.

- Regulatory patchwork: The EU and Singapore have clear frameworks. The U.S. still has overlapping oversight between the SEC and CFTC, which forces global institutions to run complex multi-jurisdictional compliance programs.

The Bottom Line

2026 is the year that digital finance stopped being a story about speculation and started being a story about infrastructure. Tokenized assets, institutional-grade custody, and multi-CBDC payment systems aren’t replacing traditional finance — they’re rebuilding it from the inside out, making it faster, cheaper, and more transparent. For financial institutions, the question is no longer whether to adopt blockchain infrastructure. It’s how fast — and whether they want to lead or follow.