Why the change?

For years, blockchain lived in two separate worlds.

On one side: crypto enthusiasts, decentralization supporters, and startups building products for a future that always seemed just around the corner. On the other hand, banks, governments, and enterprises watching cautiously from the sidelines, intrigued but unconvinced.

That divide is closing.

In 2025 and now into 2026, institutional blockchain adoption shifted from “interesting experiment” to “business priority.” Major financial institutions aren’t just running pilots anymore; they’re launching production systems. Stablecoins led this shift, tokenized assets followed, and suddenly, blockchain stopped being a future technology and became a current infrastructure.

But here’s the reality: adoption is messy. For every success story about a bank processing millions in tokenized transactions, there’s another about a pilot project that stalled after eighteen months. For every government exploring blockchain for public records, there’s a compliance barrier no one saw coming.

The institutions that are succeeding? They’re not the ones with the biggest budgets or the flashiest tech. They’re the ones who understood what institutional blockchain adoption actually requires: regulatory clarity, technical rigor, operational discipline, and the patience to build systems that work in regulated environments.

What’s Driving Adoption Forward

Three forces converged to make 2025 a turning point, and they’re playing out differently across markets.

First, regulatory frameworks finally started taking shape. After years of uncertainty, jurisdictions from the EU to Singapore to Nigeria began publishing clearer guidelines on digital assets, tokenization, and blockchain-based financial services. About 80% of reviewed jurisdictions saw financial institutions announce digital asset initiatives in 2025. When regulators provide roadmaps instead of question marks, institutions move faster.

As Hoolie Tejwani, head of Coinbase Ventures, put it: “When founders understand the rules, they build responsibly, and investors can commit with confidence.”

In Nigeria, this regulatory evolution has been particularly dramatic. After the Central Bank of Nigeria lifted its crypto ban in December 2023 and issued guidelines allowing banks to service licensed crypto firms, institutional activity exploded.

In April 2025, President Bola Ahmed Tinubu signed the Investments and Securities Act 2025, formally classifying virtual assets as securities under SEC regulation. Nigeria now has what many African markets still lack: a dedicated blockchain regulatory framework.

Second, the technology matured. Early blockchain platforms struggled with speed and scale. Today’s permissioned networks can handle enterprise transaction volumes without the energy costs or performance issues that plagued earlier systems.

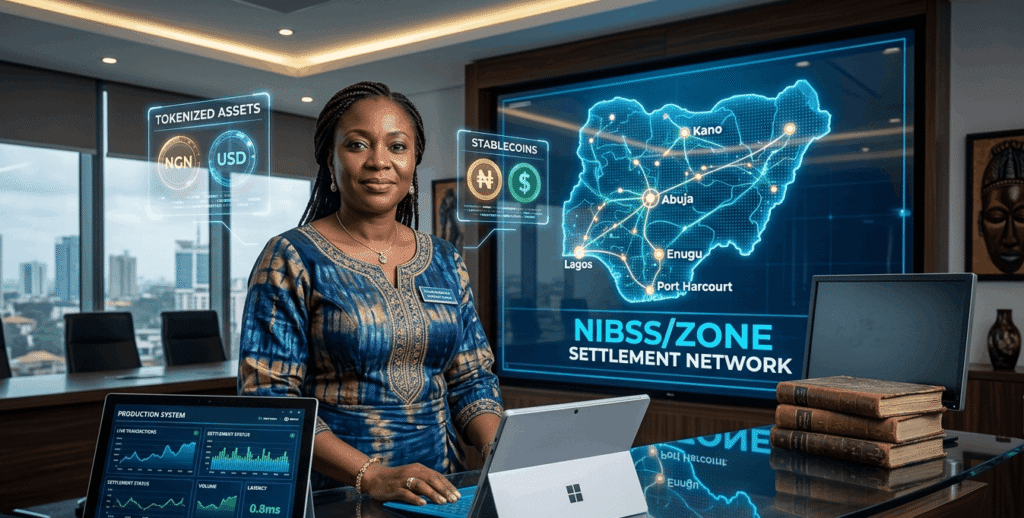

In August 2024, Nigeria Inter-Bank Settlement System (NIBSS) partnered with Zone’s blockchain network, a watershed moment for African financial infrastructure. This wasn’t a pilot; it was NIBSS integrating blockchain into the core settlement systems that power Nigerian banking. The move toward blockchain-enabled interbank settlements demonstrates how African institutions are leapfrogging traditional infrastructure upgrades entirely.

Third, the business case became undeniable. Walmart cut food safety incident response time from weeks to 2.2 seconds using blockchain for supply chain tracking. Cross-border payments that took days now settle in minutes. When ROI shows up in operational metrics, CFOs pay attention.

For African institutions, the business case is particularly compelling. Intra-African trade currently represents less than a quarter of total trade volumes on the continent. By leveraging stablecoins and tokenized trade finance, financial institutions can reduce transaction costs and improve liquidity for small and medium-sized enterprises, critical for regional economic integration.

Stablecoins deserve special mention here. They became the gateway for institutional blockchain adoption, combining the stability institutions need with the efficiency blockchain provides. Stablecoin market capitalization is expected to double in 2026 from its current level of roughly $300 billion. In Nigeria, where currency instability and inflation of over 24% have driven massive crypto adoption, stablecoins aren’t speculation; they’re survival tools that are now moving into formal banking channels.

What’s Still Holding Institutions Back

Adoption isn’t moving as fast as the headlines suggest.

The biggest barrier? Legacy systems. Most financial institutions run on infrastructure built decades ago. Integrating blockchain into these environments isn’t just technically complex; it’s organizationally exhausting.

You’re not just installing new software; you’re redesigning workflows, retraining staff, and convincing risk committees that this won’t break everything else.

This challenge is even more pronounced in African markets. As research on South African public sector blockchain readiness found, adoption is “significantly constrained by limited digital literacy, organizational resistance, and inadequate change management frameworks.” The technology might be ready, but institutions often aren’t.

Compliance costs remain steep. Building a blockchain solution might cost millions, but making it compliant with data privacy laws, financial regulations, and cross-border rules? That’s where budgets explode. Nigeria’s Data Protection Act 2023 and its implementation directive, which became effective in September 2025, added another layer of compliance requirements that blockchain systems must address. Smaller institutions often look at those numbers and decide to wait.

Then there’s the scaling problem. A pilot with 10 transactions per day is one thing. A production system handling 10,000 transactions per day while maintaining security, uptime, and regulatory compliance is entirely different. The gap between proof of concept and real deployment is where most projects die.

Research shows that 90% of blockchain initiatives fail to deliver ROI due to interoperability and adoption barriers. Even high-profile projects aren’t immune. The Maersk-IBM TradeLens platform, which reduced paperwork costs by 70-90% and decreased shipping times by 40%, was discontinued in 2022 after failing to achieve sufficient enterprise adoption.

Governance is the quiet killer. Even when the tech works and compliance is sorted, many institutions underestimate what it takes to govern a blockchain system long-term. Who makes decisions when the network needs upgrades? How do you handle disputes between participants? What happens when regulations change? Without clear answers, production systems stall.

Who’s Getting It Right

The institutions succeeding with blockchain aren’t necessarily the most innovative; they’re the most disciplined.

They start with clear business problems, not technology experiments. They’re not adopting blockchain because it’s trendy; they’re adopting it because it solves something measurable: settlement speed, transparency, and cost reduction.

They build compliance into the architecture from day one, not as an afterthought. Regulatory approval isn’t a final hurdle; it’s part of the design process. For instance, most tokenized bonds, funds, and structured products in 2025 are issued on permissioned platforms operated by banks precisely because they were built with compliance embedded.

JPMorgan extended JPM Coin functionality to public blockchains in November 2025. BlackRock expanded its European digital-asset offering with a listed Bitcoin product and continues developing tokenized bond strategies. These aren’t experiments; they’re production systems handling real institutional capital.

In Africa, institutional adoption is following a different but equally deliberate path. Kenya’s Virtual Asset Service Provider Bill of 2025 created a legal foundation for digital assets. Nigeria’s 2025 Securities Act clarified rules governing crypto assets and market conduct. South Africa’s FSCA issued 300 crypto asset service provider licenses by the end of 2025, signaling the transition from informal growth to regulated maturity.

These markets aren’t copying Western approaches; they’re building frameworks suited to African realities. The 2025 Africa Blockchain Festival in Kigali showcased how the continent is “leveraging blockchain not to replicate existing financial systems, but to build new frameworks of trust, transparency and inclusion.”

They invest in an integration strategy as much as blockchain development. The institutions that scale are the ones treating blockchain as part of their broader infrastructure, not a standalone experiment.

And critically, they recognize that adoption is a journey, not a light switch. As one industry observer noted: “In 2025, the training wheels came off. 2026 is about scaling what’s already running.” The organizations that succeed plan for this reality instead of being surprised by it.

What This Means for Institutions Today

If your organization isn’t exploring blockchain, the question isn’t whether to adopt—it’s how to adopt in a way that actually works.

The window between early mover advantage and late adoption risk is narrowing. Bitcoin and Ethereum spot ETFs accumulated $31 billion in net inflows while processing approximately $880 billion in trading volume, establishing regulated exposure vehicles as core infrastructure. Institutions that delay might find themselves competing against peers with faster settlement times, lower operational costs, and better transparency.

In Nigeria specifically, the number of active crypto users is projected to rise to 27-30 million by 2026, with institutional participation expected to accelerate as banks and fintechs receive clear licensing rules from the Central Bank. Markets move quickly when regulatory clarity arrives.

But rushing in without the right foundations, regulatory clarity, technical capability, and governance frameworks leads to expensive failures.

The institutions winning at blockchain adoption aren’t the boldest or the most cautious. They’re the ones who understand that blockchain isn’t just a technology decision, it’s a strategic shift that touches compliance, operations, technology, and business model. And it requires partners who can navigate all of those dimensions, not just write smart contracts.

For African institutions in particular, strategic success requires investing in technical and soft skills, stakeholder training, and institutional reform before blockchain can fulfill its promise of improving transparency and operational efficiency. That’s where the real work begins, and that’s what CBC is committed to doing.