There’s a quiet revolution happening in Nigeria’s financial system, and it didn’t start in a boardroom. It started on a smartphone.

While traditional banks were busy building branches, millions of Nigerians were already moving money, saving in dollars, and paying suppliers through platforms that didn’t exist a decade ago. The result? A country that skipped the slow lane of legacy finance and is now speeding down a road of its own making.

This is Nigeria’s leapfrog moment, and the numbers make it impossible to ignore.

From the Fringes to the Mainstream

Not long ago, crypto in Nigeria was largely peer-to-peer informal, unregulated, and driven by necessity. Traders bypassed banking restrictions to buy and sell digital assets, operating largely outside the formal financial system. That workaround, born out of frustration, turned out to be the seed of something much bigger.

By 2025, an estimated 22 million Nigerians, roughly 10.3% of the population, held or used cryptocurrencies. A decade earlier, that figure stood at just 0.4%. That’s not incremental growth. That’s a generational shift compressed into ten years. And the momentum isn’t slowing. The number of active crypto users in Nigeria is projected to reach 27 to 30 million by 2026, with stablecoins remaining the most popular choice for everyday transactions.

That’s not incremental growth. That’s a generational shift compressed into ten years.

Why Stablecoins, Not Speculation

It’s easy to reduce Nigeria’s crypto story to speculation and hype. That would be a mistake.

The real driver is far more practical: currency protection. The naira depreciated sharply between 2023 and early 2025, falling from roughly ₦460 to around ₦1,500 per US dollar a loss of more than 60% in value. For ordinary Nigerians, stablecoins aren’t a gamble. They serve as a financial safety net.

Stablecoins like USDT now account for 43% of retail crypto transactions under one million dollars, as households and small businesses use them to preserve purchasing power. This is financial innovation driven not by venture capital, but by lived economic reality.

The Infrastructure Is Catching Up

What makes this moment especially significant is that the formal system is now moving to meet where citizens already are.

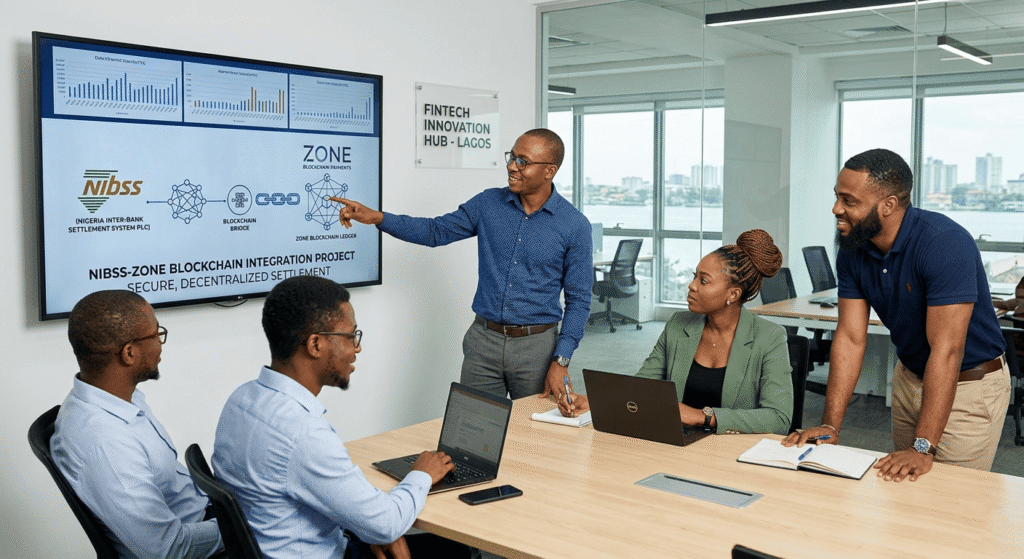

In a landmark development, the Nigeria Inter-Bank Settlement System (NIBSS) partnered with Zone’s blockchain network, modernising Nigeria’s financial infrastructure with faster, more transparent interbank settlements and reduced fraud risk.

On the regulatory front, the 2025 Nigerian Investment and Securities Act formally recognised digital assets as securities under Nigerian law, providing a legal framework for regulating crypto exchanges, platforms, and service providers. This is the regulatory clarity that serious institutional players have been waiting for.

Meanwhile, Moniepoint, a digital payments and banking platform, achieved unicorn status after securing $110 million in funding, with investors including Google, pushing its valuation beyond $1 billion. Nigeria’s fintech sector isn’t just growing. It’s graduating.

The Policy Imperative

For policymakers and industry professionals reading this, the message is direct: the architecture of Nigeria’s financial future is being built right now, with or without traditional institutions at the table.

Fintech now contributes 18.9% to Nigeria’s GDP, with that figure projected to climb further. In 2024, the country recorded over 108 billion mobile money transactions valued at $1.68 trillion. These are not niche numbers. They are macroeconomic signals.

The leapfrog opportunity is real, but it comes with responsibility. Regulators must balance openness with oversight. Industry leaders must build for inclusion, not just efficiency. And policymakers must resist the temptation to over-regulate a system that is, for many Nigerians, already working better than the one it is replacing.

Regulators must balance openness with oversight. Build for inclusion, not just efficiency.

The Bigger Picture

Nigeria is not just adopting fintech and crypto; it is demonstrating what happens when a large, young, mobile-first population meets genuine financial need. For other emerging markets grappling with currency instability, high remittance costs, and exclusion from the global financial system, Nigeria serves as a powerful case study.

The traditional banking model took generations to build and decades to reach the masses. Nigeria’s digital financial system is doing it in years.

That’s the leapfrog. And the window to shape it , thoughtfully, boldly, and inclusively, is open right now.

The question for leaders and institutions isn’t whether Nigeria’s digital finance revolution will happen. It’s whether you’ll be part of building it.